Which Telehealth Companies Sell GLP-1 Drugs in 2026? A Sourced Provider Map

There is no single “telehealth provider” for GLP-1 drugs in 2026. There are four channels, each with a different legal pathway, a different cost structure, and a different switch cost when you want to leave. The provider names on most listicles (Hims, Ro, Calibrate, Mochi, Form, Knownwell) sit across all four channels in ways the listicle format does not surface.

This article is the map. We do not score the providers here; the sibling article at compounding-providers-status-may-2026 handles current prices and warning-letter status. The upstream question we answer here: when a provider says you can get a GLP-1 through them, which of the four pathways are they using, and what does that mean for what you pay and how easily you can leave?

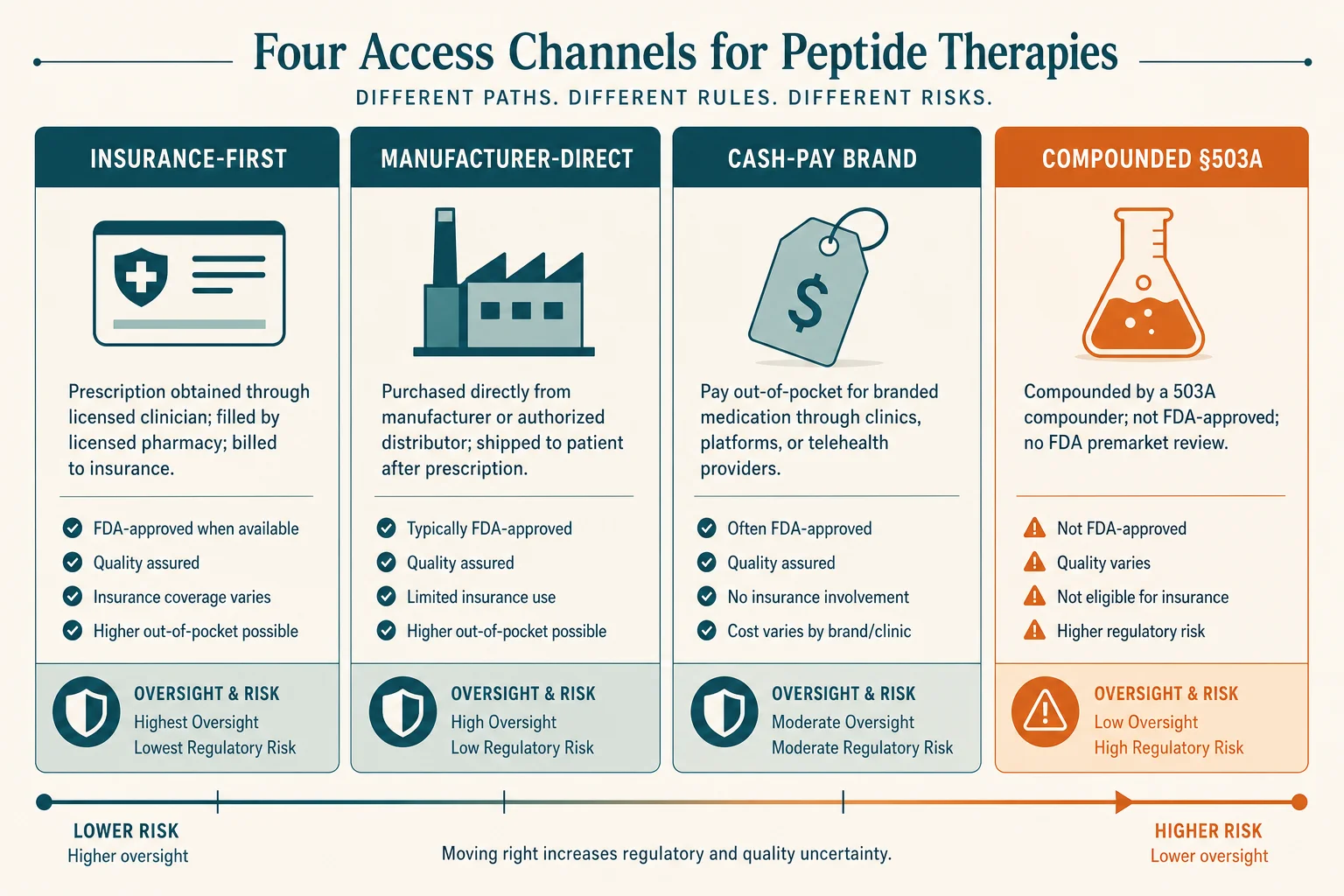

The four ways US patients access GLP-1s today

Strip away the marketing and almost every US patient is in one of four buckets.

1. Manufacturer-direct

Novo Nordisk runs NovoCare Pharmacy for Wegovy and Ozempic (NovoCare Pharmacy). Eli Lilly runs LillyDirect for Zepbound and Mounjaro (LillyDirect Zepbound). Both are pharmacy storefronts owned by the drug-maker; both ship FDA-approved product at published cash prices; neither writes prescriptions itself. You bring the script, they fulfil it.

2. Insurance-first telehealth

Calibrate, WeightWatchers Clinic, Form Health, and Knownwell are the named examples. Their core competence is running prior authorisation under your existing commercial or employer plan, so that you pay your copay rather than a cash price. They sell the program, not the drug; the drug comes from a retail pharmacy under your insurance benefit.

3. Cash-pay brand-only telehealth

Ro, LifeMD, the brand-name side of Hims & Hers, and (since September 2025) WeightWatchers and Sesame all sit here. They write a brand-name prescription and route fulfilment through NovoCare or LillyDirect. You pay cash, but you get the FDA-approved pen or vial.

4. Compounded GLP-1 telehealth

Hims (for its compounded line), Mochi Health, Henry Meds, Fella, Willow, and a tail of smaller sites still operate under FDC Act §503A(b)(1)(D), the personalised-need carve-out. The regulatory status is contested. We cover the legal posture in our compounding-cliff timeline; the prices and warning-letter status sit in compounding-providers-status.

Two adjacent models do not fit neatly. Primary-care-adjacent membership clinics (Knownwell) treat the GLP-1 as one prescription inside a longer cardiometabolic relationship. Bariatric-program-adjacent telehealth (Wondr Health) treats the drug as one tool inside a behavioural intervention. Both have a foot in the insurance-first bucket with a different sales motion.

Manufacturer-direct: NovoCare and LillyDirect

NovoCare Pharmacy and LillyDirect are the two manufacturer-owned channels — probably the lowest-friction option for many patients in 2026.

NovoCare (Novo Nordisk)

NovoCare ships Wegovy and Ozempic at published self-pay prices:

- Wegovy injection: $349/month at standard doses; $199/month introductory for new patients on the two lowest doses through June 30, 2026 (Novo Nordisk press release)

- Wegovy oral pill: $149/month for the two lowest doses

- No prescribers employed — you bring a script from your own physician or through an integrated partner (Ro, LifeMD, WeightWatchers Clinic, Sesame, Hims)

Hims & Hers was removed from the NovoCare partner list in June 2025, then re-partnered in March 2026 after settling Novo's patent suit and exiting compounded GLP-1 marketing (STAT News).

LillyDirect (Eli Lilly)

LillyDirect covers Zepbound and Mounjaro:

- Self-pay pricing: $299/month (2.5 mg starter), $399/month (5 mg), $449/month (7.5 mg and above) after the December 2025 price cut (Eli Lilly press release)

- Fulfilment: EVERSANA and Truepill

- Prescribing partners: Form Health, 9amHealth, Knownwell (Modern Healthcare)

- Walmart retail pick-up available at participating locations since October 2025

What to know about both

The advantages are clear: published prices, FDA-approved product, no platform subscription layered on top of the drug cost. The limitation is that the clinical relationship is thin, and the integrated telehealth partner is paid to convert you onto the manufacturer's product. A US Senate investigation closed in 2025 raised the influence question directly (Fierce Pharma). If you already know which drug you want, that is not a problem. If you want a clinician genuinely indifferent between Wegovy and Zepbound, it may be.

Insurance-first telehealth (program-led)

The insurance-first programs bet that the cheapest path to a year of GLP-1 therapy is your own commercial or employer plan. Patients with covered plans typically see a copay in the $25–$50/month range; the program charges a separate monthly fee (typically $99–$199) for clinical visits, prior-authorisation workflow, and coaching.

Calibrate

The longest-running insurance-first program. Sells a structured twelve-month metabolic-health program with insurance navigation as a core feature. Pricing is $199/month with a three-month upfront commitment (down from $299/month after a 2024 restructuring). The drug runs through your plan.

WeightWatchers Clinic

The post-Sequence iteration of this model. WeightWatchers acquired Sequence in April 2023 for $132 million (WeightWatchers/GlobeNewswire). After the parent's 2025 Chapter 11 reorganisation, the GLP-1 strategy tightened around brand-name product; Clinical subscribers transitioned off compounded semaglutide from May 22, 2025.

Form Health

Takes the most clinical posture of the cohort, with an American Board of Obesity Medicine clinician as lead. Also one of the three telehealth partners on the LillyDirect referral list — operating in both the insurance-first and cash-pay buckets depending on the patient's coverage.

Knownwell

The cleanest primary-care-adjacent example. Offers virtual primary care in all fifty states and in-clinic across six states. On the LillyDirect referral list; accepts commercial insurance for the visit. CVS Health Ventures led a $25 million round in 2025 (Fierce Healthcare). The GLP-1 sits inside an ongoing primary-care relationship rather than alongside a thin chat product.

For patients with employer coverage, this is usually the lowest-cost durable path. The trade-off is time: prior-authorisation cycles run days to weeks, and the per-month program fee continues whether or not the PA succeeds.

Cash-pay brand-name telehealth

The cash-pay brand-name segment is the one most patients first encounter through advertising. Ro, LifeMD, the brand-name side of Hims & Hers, Sesame, and WeightWatchers (for cash-pay tracks) all sit here. The model: a telehealth platform writes a brand-name prescription; fulfilment routes through NovoCare or LillyDirect; you pay the manufacturer's cash price plus the platform's subscription or visit fee.

The April 2025 NovoCare partnerships made this segment a meaningful share of new Wegovy starts. Hims & Hers stock jumped 23% the day the deal was announced (CNBC); a Wegovy three-month subscription was priced at $329/month, falling to $249/month for a 12-month commitment. By June 2025 the Hims arrangement was over; Ro, LifeMD, and WeightWatchers continued. Hims returned to the Novo partnership in March 2026 on brand-name-only terms.

This bucket is the one most likely to converge on identical pricing in 2026. NovoCare's posted prices are the floor; the telehealth layer charges the same price plus a visit or subscription fee. Differentiation is in platform experience (clinician access time, dose-titration messaging, whether coaching is bundled), not in the price of the molecule.

LifeMD is worth picking out: it is a membership-first platform ($19/month for LifeMD Plus, $79+/month for the Weight Management Program) where the GLP-1 is one of many medications the membership provides access to. The per-script cost is lower than a single-purpose competitor's, but the membership bundles a continuous billing relationship; the off-ramp involves cancelling the membership, not just the prescription.

Per-provider in-depth reviews for the major cash-pay and compounded platforms are on these pages: Ro Body, PlushCare, Henry Meds, Mochi Health, and Eden Health. Each applies the same five-question rubric used on this page.

Compounded-GLP-1 telehealth, in May 2026

The compounded segment has contracted substantially from its 2023–2024 peak. The regulatory timeline is at compounding-cliff-2026-timeline and the current price-and-warning-letter status is at compounding-providers-status-may-2026. Here we describe the business model and the current roster.

Who remains in May 2026. The named active platforms under §503A(b)(1)(D) are Mochi Health, Henry Meds, Fella Health, Willow, and a tail of smaller sites. Hims & Hers exited compounded GLP-1 marketing as part of its March 9, 2026 Novo Nordisk settlement. Several 503B outsourcing facilities — including ProRx and BPI Labs — ceased GLP-1 production in early 2026 under regulatory pressure. The supply chain for the remaining compounded providers has narrowed to a smaller cohort of state-licensed 503A pharmacies.

Compounded-GLP-1 telehealth sites rely on FDC Act §503A(b)(1)(D), the personalised-need exception. The exception lets a 503A pharmacist compound for an identified patient when the prescriber documents that a change from the FDA-approved product produces “a significant difference” for that patient. In practice these providers frame nearly every prescription as a personalised dose (a non-commercial dose like 1.7 mg) or a combination preparation (semaglutide with B12).

FDA and the manufacturers dispute that framing. Novo Nordisk's February 2026 patent suit named Hims & Hers, Mochi, Fella, and eleven other firms; FDA warning-letter waves in September 2025 and March 2026 targeted compounders and the marketing claims made by telehealth fronts (CNBC; Fierce Pharma).

The business model is subscription-heavy. Compounded providers price the program rather than the drug, with monthly fees of $179–$299 commonly bundling the visit, pharmacy fulfilment, and continued refills until you cancel. The combined effect (cash-pay, subscription, no insurance billing, regulatory cloud) is a price below NovoCare's $349 but a meaningfully higher switch cost than the manufacturer-direct path.

A billing pattern to know about. Patient complaints across forums document a recurring compounded-telehealth billing issue: non-refundable initiation fees charged before any consultation or service is delivered, and subscription charges that continue after the patient believes they have cancelled. The mitigation: remove your payment method from the platform before initiating cancellation, and request written confirmation. This applies across the category, not to any single provider.

The business models behind the prices

Reading this market by drug rather than by business model misses what drives your bill. Four models recur across the four channels.

Subscription billing

The dominant compounded model, increasingly common on the cash-pay brand side. A monthly fee bundles the visit, prescription, and coaching, whether or not you refill. The visible per-fill cost falls; the implicit cost of leaving rises — cancelling requires an off-platform decision, not just declining a refill.

Per-prescription billing

The manufacturer-direct model. NovoCare and LillyDirect charge per fill with no platform-level subscription. The price is transparent; the clinical support is thinner.

Bundled-with-program

The insurance-first model. The drug runs through your plan at copay pricing; the program fee covers prior-authorisation work, dietitian access, and behavioural coaching. Total monthly outlay is often the highest of the four, but the manufacturer's cash price is not part of it.

Insurance-billed visit, cash for the drug

The model the LillyDirect–Knownwell–Form partnerships have made the new default for many commercial-insurance patients. The visit runs under your plan; the drug runs cash through LillyDirect.

For an Anxious First-Timer, the durable question is not which provider but which model. Provider line-ups will reshuffle; the model determines what happens when, twelve months in, you want to taper off, an event the subscription model is structurally not designed to make easy. We cover the off-ramp at our methodology page.

What patients say actually drives the choice

Three recurring themes from r/Ozempic and r/Semaglutide document how patients actually navigate this decision — and where the frustrations concentrate.

Price ceiling matters more than channel. The question asked most often is some version of: "Is my budget even realistic long-term?" Patients without insurance typically set a ceiling around $200/month and ask whether brand or compounded can meet it. With NovoCare's introductory $199/month pricing and compounded sitting at $199–$299, the market has converged on a band those patients can reach. The decision shifts from "can I afford brand?" to "is the modest price premium for brand worth it?" — which is a different and arguably more tractable question.

Subscription fine print is the single biggest source of frustration. The most visible provider complaints involve billing practices rather than drug quality. A documented complaint pattern around Mochi Health — non-refundable upfront fees charged before any consultation was delivered, and (in multiple accounts) monthly charges continuing for months after the patient believed they had cancelled — illustrates the structural issue: subscription models are designed to make the exit difficult, and the exit is not the billing event the platform shows you at signup. Patients report losing hundreds of dollars before noticing the pattern. The mitigation is simple but rarely advertised: remove your payment method before attempting to cancel, and request written confirmation of cancellation.

Primary-care refusal is a bigger barrier than price for many patients. A recurring post pattern is: "My primary care doctor isn't very open to prescribing GLP-1s, so I'm trying to understand the safest way to go the telehealth route." This drives patients toward telehealth not because of price but because their existing clinical relationship is a dead end. For this patient, the insurance-first programs (Calibrate, Form Health, Knownwell) solve two problems simultaneously — they route around the unwilling PCP while running the prior-authorisation workflow that the PCP would otherwise handle. The manufacturer-direct channel (NovoCare, LillyDirect) solves only the second problem; the patient still needs a prescriber, and that prescriber is now a telehealth platform rather than a long-term clinical relationship.

Five things to ask any provider

A reader picking a provider in May 2026 should ask the same five questions of any of the named platforms above. The answers expose the structural-conflict points the brand websites do not surface.

-

Which of the four channels is this prescription using? Manufacturer-direct, insurance-first, cash-pay brand, or compounded. The legal posture and price floor follow from the channel, not the provider name.

-

What is the billing model? Subscription, per-script, or program bundle. Ask what happens if you skip a refill, taper a dose, or pause for a month.

-

What is the off-ramp? Specifically: at what dose can you taper, and does the provider continue the relationship through maintenance, or does the subscription assume continuous full-dose refilling?

-

Who actually writes the prescription? For LillyDirect referrals it is Form, 9amHealth, or Knownwell. For NovoCare referrals it is the partnered telehealth platform. For compounded sites it is a 503A pharmacist with prescriber sign-off. The named entity matters for any future complaint or insurance reimbursement.

-

What is your insurance posture? Direct billing, superbill, or no insurance involvement. The insurance-first programs answer this differently from the cash-pay programs; both answers are valid, but they imply different total-cost-of-care math.

The long-form rubric for working through these is on the methodology page. It is the same rubric we apply when we review any provider on this site.

What's likely to consolidate over the next 12 months

The compounded segment will get smaller. Not from a single regulatory event, but from the cumulative weight of three forces: FDA warning-letter cadence (two waves in nine months, both targeting marketing claims and compounding), manufacturer litigation (Novo's February 2026 omnibus suit named fifteen firms), and FDA's April 30, 2026 proposal to keep semaglutide and tirzepatide off the 503B bulks list permanently. Smaller compounders without the legal budget to defend personalised-dose framing exit first.

The cash-pay brand segment will converge. NovoCare and LillyDirect prices are the floor; differentiation among Ro, LifeMD, WeightWatchers, and Sesame is narrowing to platform UX, support, and clinician access time. Expect price uniformity within twelve months and consolidation by 2027.

The insurance-first segment will pick up share from both other cash-pay segments, especially if employer GLP-1 coverage expands meaningfully from the 19% baseline reported in 2025 employer-benefits surveys. The acquirers most likely to be active here are insurers and large primary-care groups.

The manufacturer-direct channels will keep growing. By Q2 2025, ~35% of new Zepbound prescriptions were already fulfilled through LillyDirect (CNBC). The October 2025 Walmart retail-pickup extends the channel to patients who would rather collect from a pharmacy than wait for shipping. The strategic question Novo and Lilly are deciding is how much further to vertically integrate before they cannibalise their own retail distribution.

How we keep this article current

This map is rechecked monthly. Three things move faster than the rest:

- Provider line-ups. NovoCare's telehealth partner list changed twice in twelve months. Compounded-segment exits will continue through 2026 — at least one named provider in this article will have wound down its compounded line by the time you read it.

- Manufacturer pricing. LillyDirect cut Zepbound vial prices in December 2025 and again in early 2026. Novo's introductory $199/month offer is scheduled to expire June 30, 2026 and may or may not be extended.

- Regulatory developments. The Senate investigation into manufacturer-direct platforms (closed September 2025) has not yet produced legislation; if it does, the LillyDirect–Form–Knownwell referral model will need to be rebuilt.

If you spot a provider missing from a channel, a partner relationship that has ended, or a price that has moved, please email [email protected]. We acknowledge corrections within five business days and publish the resolution within fifteen.

Frequently asked questions

What are the four main ways to get a GLP-1 drug in the US in 2026?

Manufacturer-direct (NovoCare for Wegovy/Ozempic; LillyDirect for Zepbound/Mounjaro); insurance-first telehealth that runs prior authorisation on your existing plan (Calibrate, WeightWatchers Clinic, Form Health, Knownwell); cash-pay telehealth reselling brand-name product through NovoCare or LillyDirect (Ro, LifeMD); and compounded-GLP-1 telehealth under §503A(b)(1)(D) (Hims, Mochi, Henry Meds, Fella). Each pathway has a different price, switch cost, and regulatory posture.

Is NovoCare Pharmacy a telehealth provider?

No. NovoCare is a fulfilment pharmacy run by Novo Nordisk. It does not write prescriptions; a valid Wegovy or Ozempic script from your own prescriber is required. Several telehealth platforms (Ro, LifeMD, WeightWatchers Clinic) integrate with NovoCare so prescription and fulfilment happen in one flow, but the prescribing clinician is on the telehealth side, not at Novo Nordisk.

Is LillyDirect a telehealth provider?

Partly. LillyDirect is Eli Lilly's direct-to-consumer site, including Zepbound vials. Prescribing runs through independent partners (Form Health, 9amHealth, Knownwell); pharmacy fulfilment runs through EVERSANA and Truepill. A 2025 Senate investigation raised questions about whether the manufacturer-funded referral arrangement influences prescribing behaviour.

Who still sells compounded GLP-1s in 2026?

A smaller cohort than two years ago, all relying on FDC Act §503A(b)(1)(D) personalised-dose framing. The named providers include Hims & Hers, Mochi Health, Henry Meds, Fella Health, and several smaller sites. Most face active litigation from Eli Lilly or Novo Nordisk, FDA warning letters, or both. Status tracked at [Compounding Providers Status](/regulatory/compounding-tracker).

What is the difference between a subscription model and a per-prescription model?

A subscription provider bills you monthly whether or not you refill, usually bundling the prescription, clinician visits, and coaching. A per-prescription model charges only when you fill but lacks the bundled support. Subscriptions reduce visible per-fill cost but raise the cost of leaving; per-prescription models are easier to leave but offer thinner support.

Which providers bill insurance directly versus give you a superbill?

Direct billing is most common with insurance-first programs (Calibrate, Form Health, Knownwell, WeightWatchers Clinic). Cash-pay telehealth (Ro, LifeMD, Hims) does not bill insurance for the medication; they sell brand-name product at a cash price through NovoCare/LillyDirect, or sell compounded product outside insurance entirely. Superbills are offered by some cash-pay providers but rarely reimbursed for weight-loss drugs without prior authorisation.

Does my employer plan likely cover Wegovy or Zepbound?

Coverage for the weight-loss indication is uncommon. A 2025 employer-benefits survey published by KFF found only about 19% of large employer plans covered GLP-1s for weight loss. Diabetes-indication coverage (Ozempic, Mounjaro) is widespread. Commercially insured patients should start with an insurance-first program (Calibrate, Form Health, Knownwell). Decision tree at [our methodology page](/methodology).